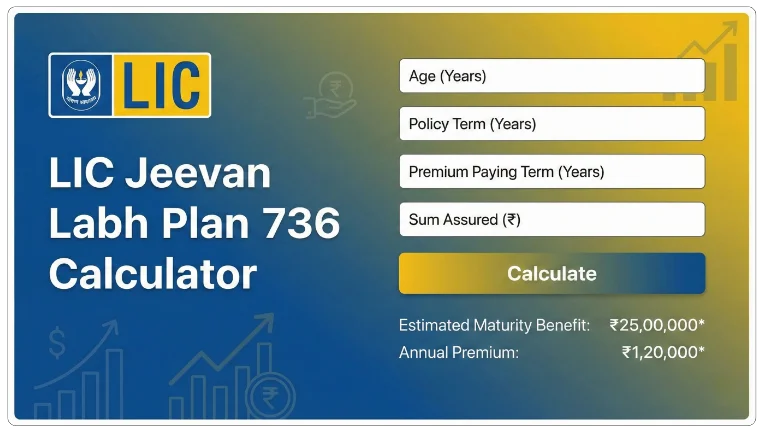

LIC Jeevan Labh Plan 736 Calculator

Plan No: 736 | UIN: 512N304V03

Launch Date: 1st October 2024

Status: Currently Available

Plan Type: Non-Linked Endowment Plan with Profit

Minimum Sum Assured: ₹2,00,000 | Maximum: No Limit

Maximum Maturity Age: 75 Years

Your Premium & Benefit Details

Estimated Maturity Benefit

*Including estimated bonuses (Subject to declaration by LIC)

LIC Jeevan Labh Plan 736 is one of those insurance plans that many families in India turn to for a mix of life cover and savings. Launched on October 17, 2024, this plan from Life Insurance Corporation of India (LIC) replaced the older version and is still active with no withdrawal date announced.

What Makes LIC Jeevan Labh Plan 736 Special?

Think of it like planting a tree today that grows steadily, giving shade to your family even if you’re not around. This is a limited premium paying endowment plan, meaning you pay for a shorter time but get protection for longer. It’s designed for people who want guaranteed returns plus bonuses, all under one policy.

The plan participates in profits, so you earn bonuses declared by LIC each year. It’s simple for salaried folks, self-employed people, or even parents saving for kids’ future. Minimum entry age is 8 years, making it great for child plans too.

Key Features You Should Know

Here are the main highlights that set Jeevan Labh 736 apart from others:

- Limited Premium Term: Pay for 10 years (16-year policy), 15 years (21-year policy), or 16 years (25-year policy).

- Flexible Terms: Choose 16, 21, or 25 years total policy duration.

- High Sum Assured Rebates: Bigger coverage means lower premiums per lakh.

- Loan Option: Borrow against your policy after 2 years’ premiums.

- Riders Available: Add accidental death or term assurance for extra protection.

These features make it flexible for different life stages, like young professionals or mid-career families.

Eligibility Criteria at a Glance

Not everyone qualifies, but the rules are straightforward. You need to be between 8 and 59 years old (depending on term), with maximum maturity age of 75. Minimum basic sum assured is ₹2 lakhs, no upper limit, in multiples of ₹10,000 up to ₹4.5 lakhs, then ₹25,000.

| Eligibility Factor | Details |

|---|---|

| Minimum Entry Age | 8 years (completed) |

| Maximum Entry Age | 59 years (16-yr term), 54 (21-yr), 50 (25-yr) |

| Minimum Sum Assured | ₹2,00,000 |

| Maximum Maturity Age | 75 years |

This table helps quick checks before buying.

How Premiums Work and Rebates

Premiums depend on your age, sum assured, term, and payment mode. Pay yearly, half-yearly, quarterly, monthly via ECS, or single (not always). Good news: rebates lower your cost.

- Mode Rebate: 2% for yearly, 1% half-yearly.

- High Sum Assured Rebate: Starts from ₹5 lakhs (2% of premium), up to 3% for ₹10-14.9 lakhs.

For example, a 30-year-old buying ₹5 lakhs cover for 16 years might pay around ₹40,000-50,000 yearly (excluding GST, approximate). Use official calculators for exacts.

Sample Premium Table for a 30-Year-Old Male (16-Year Term)

Here’s an illustrative table based on standard rates (premiums exclude GST and rebates; actuals vary).

| Basic Sum Assured (₹) | Yearly Premium (Approx.) | With High SA Rebate (if applicable) |

|---|---|---|

| 2,00,000 | ₹28,500 | No rebate |

| 5,00,000 | ₹68,000 | ₹66,640 (2% rebate) |

| 10,00,000 | ₹1,30,000 | ₹1,26,100 (3% rebate) |

These are estimates; check LIC’s premium calculator for precision.

Maturity Benefit: What You Get at the End

If you survive the term, you receive the Basic Guaranteed Sum in addition to the Simple Reversionary Bonuses + Final Additional Bonus (FAB, if declared). Bonuses depend on LIC’s performance, often ₹50-55 per ₹1,000 sum assured yearly (illustrative).

For a ₹5 lakhs policy over 16 years, maturity could be ₹8-10 lakhs or more with bonuses (at 8% illustrative rate). It’s tax-free under Section 10(10D).

Death Benefit: Protection for Your Family

In case of death, nominee gets the higher of:

- Basic Sum Assured, or

- 7 times Annualised Premium,

Plus bonuses and FAB. Minimum 105% of total premiums paid. This ensures no loss for family.

Example: If annual premium ₹50,000, 7x is ₹3.5 lakhs minimum, but higher if sum assured is more.

Optional Riders to Boost Coverage

Enhance with these at extra cost:

- Accidental Death & Disability (AD&D) Rider.

- New Term Assurance Rider (inception only).

No critical illness in 736, unlike older versions.

These add value without much premium hike.

Why Use LIC Jeevan Labh Plan 736 Calculator?

Calculators make planning easy. Enter age, term, sum assured, and get premiums, maturity, death benefits instantly. Sites like liccalculator.xyz offer free tools mimicking LIC’s logic, with illustrations at 4% and 8% rates.

Official LIC site has premium calculators too: LIC Premium Calculator. Third-party ones like Policybazaar’s help compare.

Pro Tip: Always verify with LIC agent for exact quotes, as bonuses aren’t guaranteed.

Step-by-Step: Using the Calculator Effectively

- Pick your age and policy term.

- Choose sum assured (start with ₹5-10 lakhs).

- Select a premium paying term (auto-linked).

- Add riders if needed.

- View maturity/death projections.

It shows year-wise breakdowns, helping decide if it fits your budget. Great for LIC agents creating proposals.

Real-Life Example: Planning for Child’s Education

Raj, 35, buys ₹10 lakhs cover (21-year term, 15-year pay). Yearly premium ~₹1.2 lakhs (post-rebate). Maturity after 21 years: ~₹18-20 lakhs (illus.). Covers kids’ college fees nicely.

Tax Benefits That Save You Money

- Premiums deductible u/s 80C (up to ₹1.5 lakhs).

- Maturity/death benefits tax-free u/s 10(10D) if premium <10% of sum assured.

Perfect for tax planning alongside savings.

Loan and Surrender Options

Need cash? Loan after 2 full years’ premiums (up to 90% of surrender value). Surrender after 2-3 years possible, but better to continue for bonuses. Grace period: 30 days.

Comparison with Older Versions

| Feature | Plan 736 (New) | Plan 936 (Withdrawn Oct 2024) |

|---|---|---|

| Launch | Oct 17, 2024 | Feb 1, 2020 |

| Death SA Multiple | 7x Annual Premium | 10x Annual Premium |

| Riders | Limited | More options (Critical Illness) |

| Loan After | 2 years | 2 years |

736 has stricter death benefit but high rebates.

Is It Worth Buying in 2026?

Yes, if you want safe, guaranteed returns (5-7% effective post-bonuses). Not for high-risk investors seeking 12%+. Ideal for conservative savers.

Common Mistakes to Avoid

- Ignoring rebates – choose high SA.

- Forgetting GST (4.5% first year).

- Buying without a calculator, overpaying is possible.

Consult agent always.

Frequently Asked Questions (FAQ)

What is the minimum premium for LIC Jeevan Labh 736?

Around ₹25,000-30,000 yearly for base cover, depending on age.

Can I buy it for my child?

Yes, from 8 years old.

Are bonuses guaranteed?

No, illustrative only.

How to calculate exact maturity?

Use the online LIC Jeevan Labh Plan 736 calculator on liccalculator.xyz or the official site.

Is there a free-look period?

Yes, 15 days to cancel.

Conclusion

LIC Jeevan Labh Plan 736 combines protection, savings, and tax perks perfectly for Indian families. Use the calculator to tailor it to your needs, and pair it with LIC agent advice. Start planning today for a secure tomorrow; it’s simple, reliable, and rewarding.